Ghost Town Markets: Why Tokenized Assets Still Can't Find Buyers

Trillions of dollars in real-world assets are theoretically addressable by tokenization. Issuance platforms have multiplied. Institutional names like Apollo, BlackRock, and WisdomTree have entered the arena. The rails exist, the assets are on-chain, and the legal wrappers are getting more sophisticated by the quarter.

But visit most tokenized asset markets on any given Tuesday afternoon, and you'll find the same thing: nothing happening. Order books thinner than a testnet. Liquidity that wouldn't fill a kiddie pool. Welcome to the ghost town.

We recently hosted episode 2 of our “Protocol Roundtable” series with leaders from Pharos, Centrifuge, Boba Network, Base, and DIA to dig into why secondary markets for RWAs remain so thin, and what it will actually take to change that. The conversation surfaced hard truths that the "tokenize everything" crowd tends to skip over.

Issuance Won the Battle. Liquidity Lost the War.

The industry has gotten good at putting assets on-chain. Tokenization infrastructure is no longer the bottleneck. What's missing is what comes after: functioning markets where those tokens actually trade, where capital can enter and exit without a phone call to the issuer.

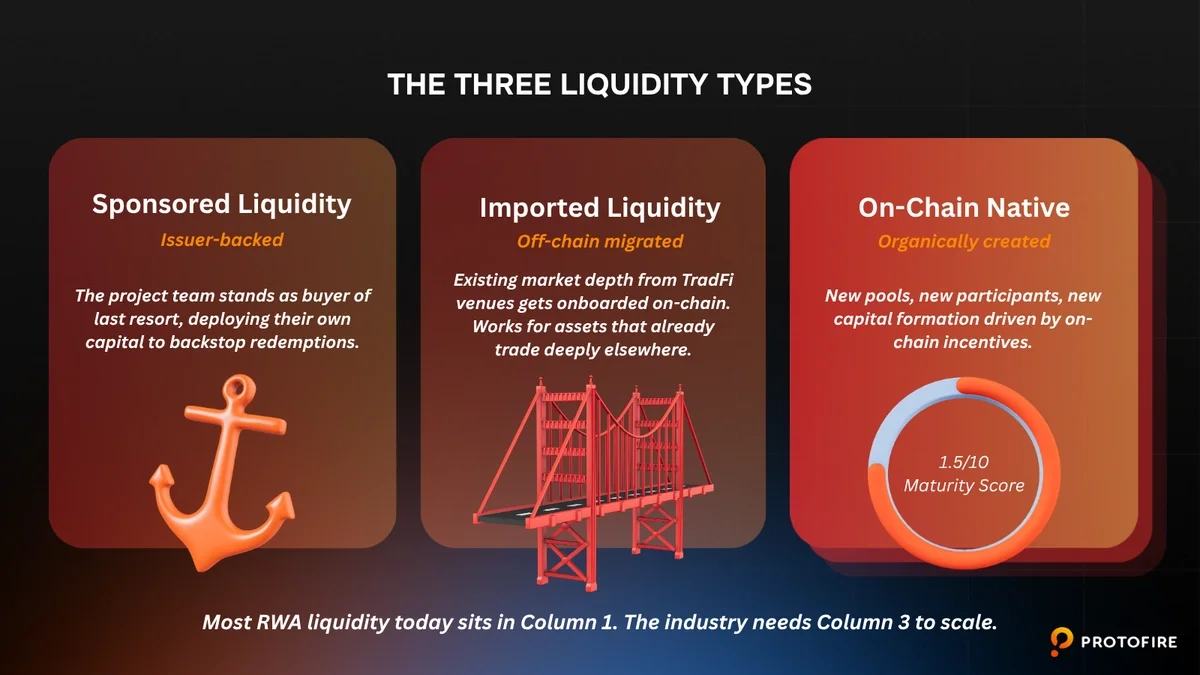

Secondary liquidity for RWAs today breaks down into three categories. The first is sponsored liquidity, where the issuer stands as buyer of last resort, deploying their own capital to backstop redemptions. Common, expensive, doesn't scale. The second is imported off-chain liquidity, where existing depth from traditional venues gets onboarded. This works for assets that already trade deeply elsewhere, but it's limited by definition. The third is organically created on-chain markets: new pools, new participants, new capital formation. On a maturity scale of one to ten, this category sits at maybe 1.5.

The industry shifted from "can we tokenize it?" to "now what?" faster than anyone built the infrastructure to answer.

Not Everything Needs a Market

One of the more honest moments in the conversation was the acknowledgment that not all tokenized assets should be liquid. It sounds counterintuitive in a space obsessed with composability and 24/7 trading, but the logic holds.

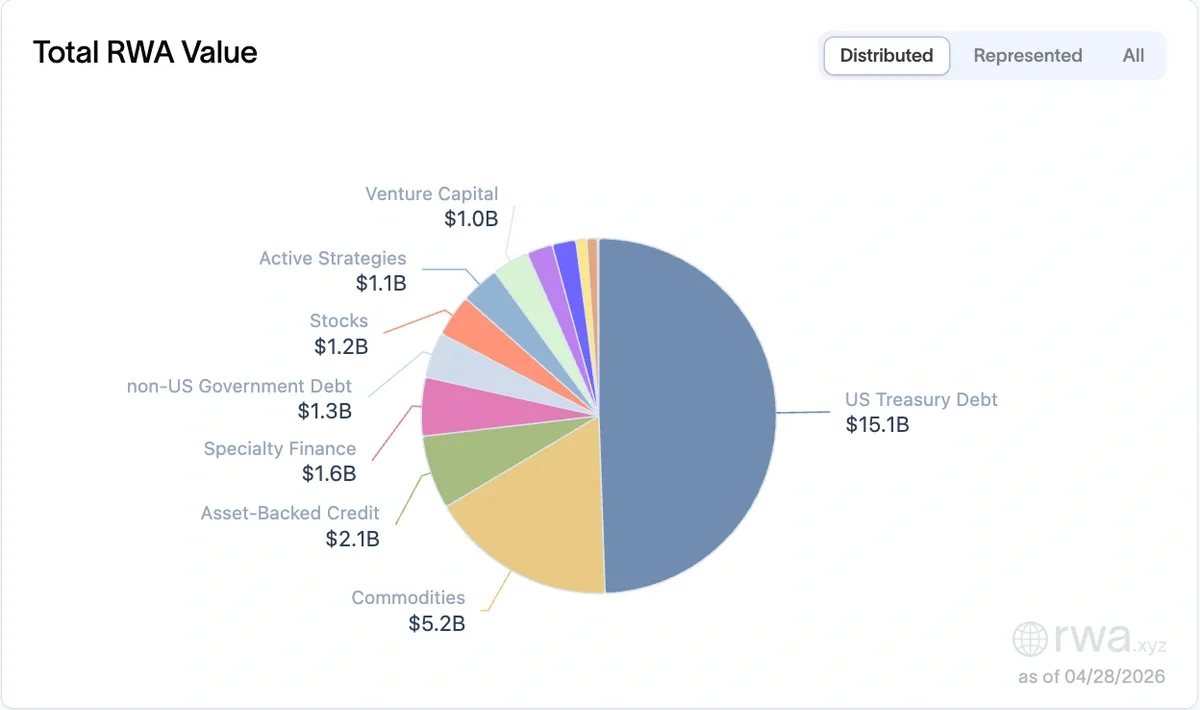

Source: RWA.xyz

Tokenized real estate and luxury goods are inherently illiquid off-chain. Putting them on a blockchain doesn't magically generate buyer demand. Tokenization might serve other purposes here: fractional access, programmable ownership, transparent provenance. But expecting a vibrant secondary market for tokenized commercial property is premature. Liquid underlyings like treasuries and high-grade credit have a realistic path to on-chain markets. Illiquid underlyings need a different playbook, one focused on access and utility rather than trading velocity.

The Pricing Problem Nobody Has Solved at Scale

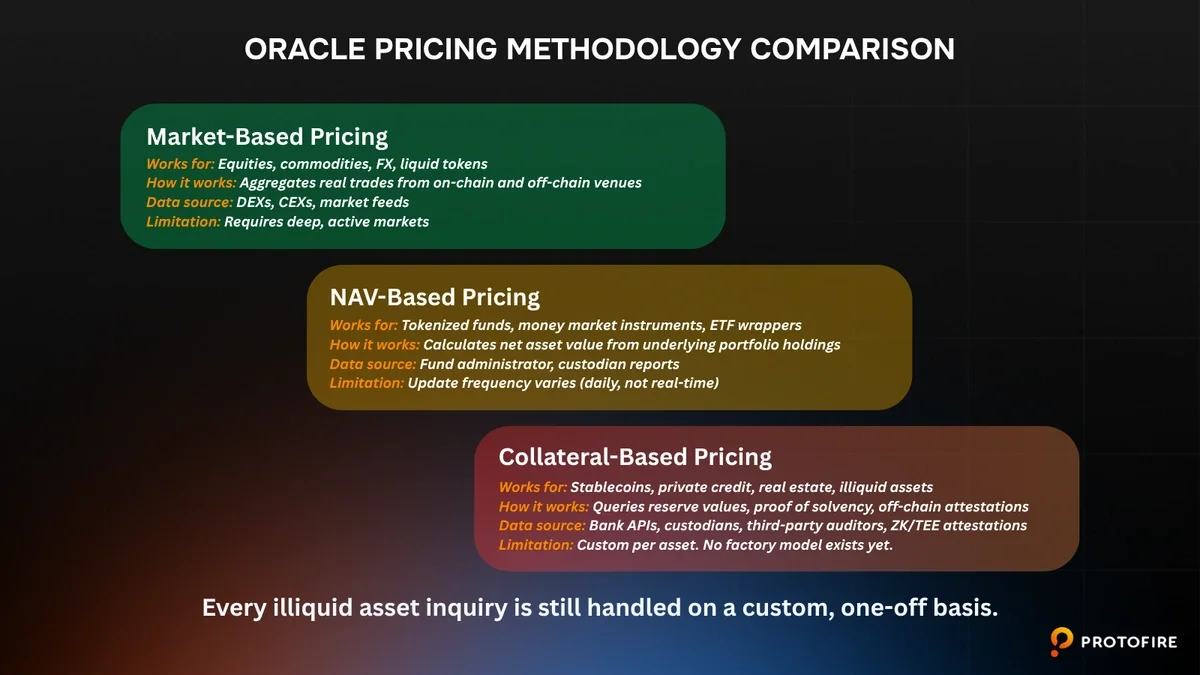

Before you can trade something, you need to know what it's worth. For liquid assets with deep off-chain markets, this is relatively straightforward. For everything else, it's a mess.

Traditional oracle models aggregate market trades. That works when there's a functioning market to aggregate. For illiquid RWAs, pricing requires entirely different methodologies: net asset value calculations, collateral ratio assessments, redeemability analysis, off-chain reserve verification. Each approach introduces its own trust assumptions.

The uncomfortable reality is that every illiquid asset inquiry is still handled on a custom basis. Where does the collateral sit? Who custodies it? Is the valuation sourced from a bank API or a stamped PDF? The industry wants a "factory model" for pricing, something repeatable and scalable. It doesn't have one yet. Each deal is bespoke, each integration is manual.

This isn't just an oracle problem. It's a structural bottleneck. Without reliable, continuous pricing, you can't build lending markets, enable liquidations, or attract market makers who need confidence in the numbers before deploying capital.

The $30 Trillion Question: Who Provides the Liquidity?

Even with pricing solved, the capital formation problem remains. Someone has to stand on the other side of every trade, and right now, the incentives are insufficient.

Capital is scattered across chains, protocols, asset types, and jurisdictions. Market makers comfortable in crypto-native markets have little reason to extend into thinly traded tokenized credit with uncertain redemption timelines. LPs face duration mismatches: they want flexibility, but underlying assets lock capital for months or years.

Some early models are attacking this creatively. Protocols are experimenting with structured liquidity pools that compensate LPs for absorbing duration risk. Issuers are wrapping long-tenor instruments into shorter redemption windows. And the BUIDL-Wintermute partnership on Uniswap showed that pairing a tokenized fund with an established market maker can bootstrap initial depth.

Yield-bearing assets also contain a built-in demand inducer. When prices drop, yields rise. At some discount, the yield becomes attractive enough that buyers show up. It's not a complete solution, but it's the kernel of how real markets form.

Institutions Are Coming, But They're Picky

Institutional allocators have started engaging with tokenized assets, but their requirements are non-negotiable: high-quality, understandable assets with near-instant liquidity. T+0 or T+1 at most. No one is locking institutional capital for 12 months in an on-chain vehicle without deep exit liquidity.

This pushes the market toward a barbell. On one end, tightly controlled environments like BUIDL's whitelisted Uniswap pool with vetted market makers. On the other, breakthroughs like WisdomTree's 24/7 trading exemption, which opens something resembling traditional cash management. Both extremes work. Neither scales.

BUIDL AUM on Ethereum. Total AUM across all chains exceeds $2.5B. Source: Dune Analytics (@0xbrokoli)

The regulatory dimension complicates things further. Tokenized private credit is likely a security in most jurisdictions. The creative response has been structural: wrapping securities into certificates or other instruments that carry different legal properties while maintaining economic exposure. It works, for now, but it's held together with legal engineering rather than regulatory clarity.

What Has to Happen in the Next 12 to 24 Months

The roundtable converged on a few conditions that need to materialize before secondary RWA markets become real.

First, 24/7 pricing. If assets trade around the clock on-chain but can only be reliably priced during traditional market hours, the entire DeFi stack on top operates on stale data. This isn't a nice-to-have. It's foundational.

Second, better data pipelines for off-chain asset valuation. The custom, one-off oracle integrations of today need to evolve into standardized frameworks with multiple data providers, attestation methods, and aggregation layers.

Third, structured capital formation. The industry needs aggregated pools where investors earn risk-adjusted returns for supplying market depth. DeFi invented the liquidity pool model. It needs to reinvent it for assets with real-world complexity.

And finally, honest asset selection. Not every tokenized instrument deserves a secondary market. Concentrating infrastructure on asset classes that can actually support trading depth will produce better outcomes than spreading thin across every tokenizable thing.

The Missing Layer

RWAs aren't failing. They're unfinished. The issuance layer works. The legal wrappers are maturing. Institutional interest is genuine. But between "asset on-chain" and "functioning market," there's a gap the industry has only begun to address.

Secondary liquidity is what turns tokenized assets from static records into productive capital. Without it, tokenization remains a filing system with better technology. Building that layer is the engineering challenge that defines whether RWAs deliver on their promise or remain ghost towns with nice architecture.

At Protofire, this is the infrastructure we build. Not tokenization for its own sake, but the financial engines and liquidity solutions that make on-chain assets actually work.